Hi Friends -

Just a quick update on what I am doing with this system.

I am focusing on testing several things:

1. How does the system perform over a longer period of time without any modification to the trading rules or the method for determining the "trade side"?

I am currently finishing a more detailed walk forward test of the system including 13 major pairs reaching back to 2001. I am not yet finished, but the preliminary results seem to show in every case that the system works as expected without any modification to the current trading rules. I'll discuss this later, but depending on the timeframe used to calculate the trade side, it seems that the returns can vary widely ... though they are still very positive.

2. Without any modification to the current trading rules, is there a more optimal way of dynamically determining the "trade side" that would have performed well over the past 7 years?

If the system can switch trade sides during major trend changes or protracted retracements, the returns can be dramatically improved. I am looking at various uncomplicated ways to do this. Any suggestions would be appreciated. Even without changing the current method of determining the trade side, the system would have performed very well over the past 7 years (01-07), to the tune of hundreds of pips per month. But it is easy to see that switching sides during major retracements or more quickly responding to major trend changes can make a big difference, perhaps even doubling or tripling the returns.

3. Beyond this, I am giving extra attention to the issue of drawdowns in the equity curve. Overall, the system appears to be very profitable, but I believe that the equity curve can be significantly smoothed by diversification and optimization.

As I mentioned before, I am trying to look first at factors other than optimizing the system rules or adding indicators, filters, etc etc etc. Afterwards, if the system seems to be robust over time, then I will see if it can be improved with optimized entry/exit rules, stops, position sizing, etc.

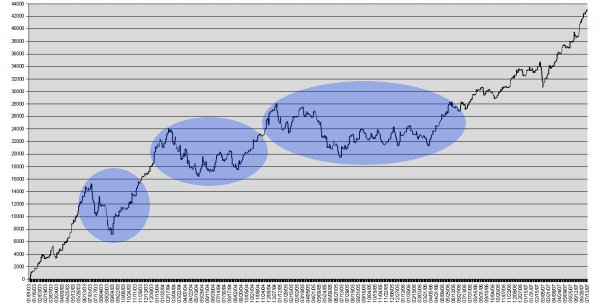

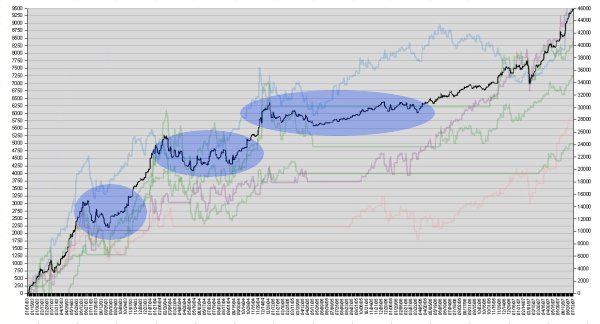

So right now, I am working on smoothing the equity curve by diversification: market diversification, system diversification, and portfolio diversification. I'm concentrating on portfolio diversification, meaning that over time the pairs this system trades will change. Managing a portfolio of pairs with simple rules for switching between pairs could improve the quality of returns and generate a smoother equity curve. I am working on something I call "hypothetical component equity curves" which I think may work. If it doesn't work ... well, I've had plenty of stupid ideas. Anyway, a picture is worth a thousand words, so let me post just a rough cut of what I'm talking about, and then I'll clarify.

Just a quick update on what I am doing with this system.

I am focusing on testing several things:

1. How does the system perform over a longer period of time without any modification to the trading rules or the method for determining the "trade side"?

I am currently finishing a more detailed walk forward test of the system including 13 major pairs reaching back to 2001. I am not yet finished, but the preliminary results seem to show in every case that the system works as expected without any modification to the current trading rules. I'll discuss this later, but depending on the timeframe used to calculate the trade side, it seems that the returns can vary widely ... though they are still very positive.

2. Without any modification to the current trading rules, is there a more optimal way of dynamically determining the "trade side" that would have performed well over the past 7 years?

If the system can switch trade sides during major trend changes or protracted retracements, the returns can be dramatically improved. I am looking at various uncomplicated ways to do this. Any suggestions would be appreciated. Even without changing the current method of determining the trade side, the system would have performed very well over the past 7 years (01-07), to the tune of hundreds of pips per month. But it is easy to see that switching sides during major retracements or more quickly responding to major trend changes can make a big difference, perhaps even doubling or tripling the returns.

3. Beyond this, I am giving extra attention to the issue of drawdowns in the equity curve. Overall, the system appears to be very profitable, but I believe that the equity curve can be significantly smoothed by diversification and optimization.

As I mentioned before, I am trying to look first at factors other than optimizing the system rules or adding indicators, filters, etc etc etc. Afterwards, if the system seems to be robust over time, then I will see if it can be improved with optimized entry/exit rules, stops, position sizing, etc.

So right now, I am working on smoothing the equity curve by diversification: market diversification, system diversification, and portfolio diversification. I'm concentrating on portfolio diversification, meaning that over time the pairs this system trades will change. Managing a portfolio of pairs with simple rules for switching between pairs could improve the quality of returns and generate a smoother equity curve. I am working on something I call "hypothetical component equity curves" which I think may work. If it doesn't work ... well, I've had plenty of stupid ideas. Anyway, a picture is worth a thousand words, so let me post just a rough cut of what I'm talking about, and then I'll clarify.