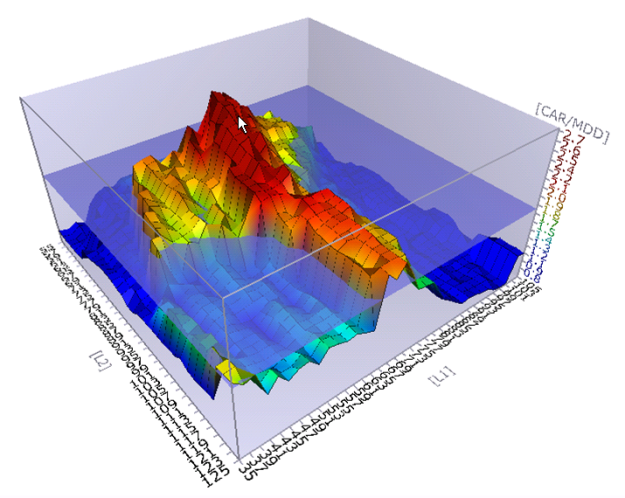

I developed an EA that has some simple parameters, and watching some youtube videos on backtesting/optimizing seems to point to the best scenario being one setting for all 12 pairs that I'm trading. Problem is I'm having difficulty finding a setting that works on all 12 pairs for the 5 year backtest.

I can, however, optimize each pair positively. My concern is that having 12 different settings for 12 different pairs may mean that I've curve fitted. I guess I'm just paranoid about curve fitting, which is why I only really have a few parameters...mainly on the ratios between SL and TP, and a couple of filters.

Or am I being paranoid?

I can, however, optimize each pair positively. My concern is that having 12 different settings for 12 different pairs may mean that I've curve fitted. I guess I'm just paranoid about curve fitting, which is why I only really have a few parameters...mainly on the ratios between SL and TP, and a couple of filters.

Or am I being paranoid?