Warren Forex http://www.forexfactory.com/images/s...ser_online.gif

Warrenforex

Member Since Sep 2006

Posts: 921

http://www.forexfactory.com/images/icons/icon14.gif Morning Report From Saxo Bank !!!

WWW.SAXOBANK.COM

Published: Jun. 20 2008, 06:46 GMT[/font]

Record retail sales shocker triggers massive GBP short squeeze. SNB decision to leave rates unchanged sends CHF tumbling.

USD continues to trade in no-man's land. Which way for USDCAD - renewed rally or more range trading?

MAJOR HEADLINES – PREVIOUS SESSION

- US Jun. Philly Fed out at -17.1 vs. -10 expected and -15.6 in May

- Germany May Producer Prices out at 1.0% MoM vs. 0.9% expected and 1.1% in Apr.

THEMES TO WATCH – UPCOMING SESSION

Key Risk Events (All times in GMT)

- Switzerland May Producer and Import Prices (0715)

- Canada Apr. Retail Sales (1230)

- Norway Norges Bank's Gjedrem to speak (1430)

Market Comments

We're running out of anything interesting to say on the short term view on the market as many currency pairs can't seem to shake off the ranges. Bond market yields remain the dominant macro story and keep marching ever higher, providing ammunition for CHF and JPY sellers against the higher yielders. The SNB non-hike yesterday sent the CHF reeling after recent signs of strength. Meanwhile, major financial stocks are closing in on their March lows (which was previously associated with bond strength and JPY & CHF weakness). But the risk-aversion crowd has been cowed into submission by the inflation and rate differential obsession. AUDJPY, for example, has closed higher in 10 of the last 12 weeks and this week will make it 11 for 13 barring an ugly sell-off today. Yet AUD rates have hardly moved against Japanese 2-year rats over the last 10 days - is this trend getting overdone. Seems like it might be time for JPY call options again... Yesterday, the German 10-year traded at a new 1-year high and is close to the 2007 peak in rates. German 2-year yields are now their highest since 2000.

The European yield curve has flattened violently since the March 17 (post Bear Stearns rescue weekend) lows in yields, with the 2-year yield rising an amazing 170 basis points and the 2-10 spread moving slightly into inversion territory. This is a classic pre-recession warning sign and is certainly putting pressure on the EuroZone financial system. Also getting much attention of late is the increasing yield spread between German bonds and bonds from areas of the EuroZone under economic duress, like Italy and Greece. In mid-summer 2007, the yield spread between Italian 10-years and German 10-years was around 20 bps, this has now widened to about 50 bps, and the same comparison for Greek 10-year bonds is approaching 70 bps. This for countries with the same currency and central bank! The potential for internal strife in the EuroZone is a story worth watching in coming months.

The UK Retail Sales number was a true shocker, with the release representing a several standard deviation surprise and the highest month-on-month change ever. The warmest May in UK history was credited with sending the cash and credit strapped consumer out in droves to buy summer clothes and more food. This is certainly a remarkable sign of resilience from the UK consumer, but the writing is on the wall in the bigger picture for the UK, so any further strength in GBP may be of fairly limited scope. The market was clearly not prepared for the strong data and the very large reaction showed that the market was likely already very short GBP upon the release and was sent running for the exits. EURGBP is now nearing its first big support at 0.7833 and below that we have 0.7765. GBPUSD has been a hopeless mess for some time. While the action yesterday saw the pair close a hair above the 55-day moving average, there has been no real trend for months. The 200-day moving average has eased lower and stands at approximately 2.0000.

The calendar is rather vacant today. Stock market action may be important with many financials and the S&P close to important lows. The market is also likely anticipating what the Fed will have to say at next Wednesday's FOMC meeting after Bernanke managed to become both more hawkish and then dovish over the last week or so.

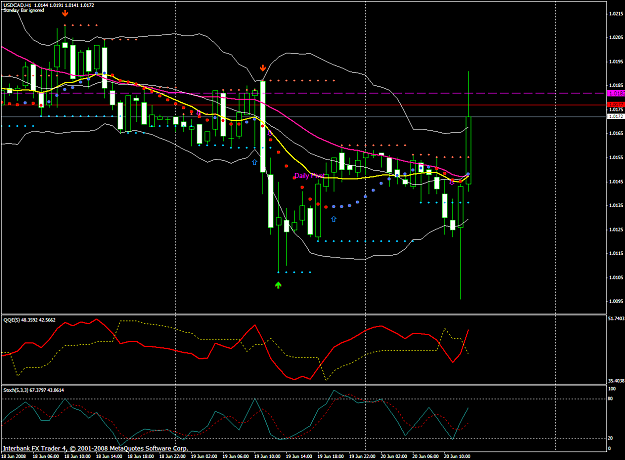

Chart: USDCAD

Here's another USD chart at risk of falling back into the range after showing promising signs of USD strength recently. USDCAD has been trading in a wide range for some 7 months now. The recent rally gave hope that the upside resistance area would give way and a real uptrend could commence. Ugly US data and a no-cut surprise from the Bank of Canada have kept the pair rangebound, however. Relative valuation and the continued US/Canada recoupling story support a move higher. On the other hand, oil probably needs a steeper sell-off to give the pair a helping hand, and the interest rate differentials have also been mired in a range for some time as well. Current levels would seem to be a pivot area for either strong support to be found for a test higher, or for a swoon back toward parity and possibly below. We still favor an eventual upside breakout, but timing is difficult with such chronic rangebound behaviour. The latest Retail Sales figures are on tap for today from Canada.

Last edited by Warren Forex, Today 6:49am Reason: To Correct Font !